Recently, interest has been growing in converting existing Feed-in Tariff (FIT) renewable energy projects to the Feed-in Premium (FIP) scheme while simultaneously installing battery energy storage systems (BESS).

Several factors are driving this trend, including the Japanese government’s policy of encouraging FIT-to-FIP conversion, the increasing frequency of renewable energy curtailment in regions such as Kyushu, and the need to secure revenues after the expiration of FIT contracts.

At the same time, many project owners are asking a fundamental question: Does it really make economic sense?

To explore this issue, we conducted a case study comparing the economics of an existing rooftop solar project in the Kyushu region under two scenarios: continued operation under FIT and conversion to FIP with battery storage.

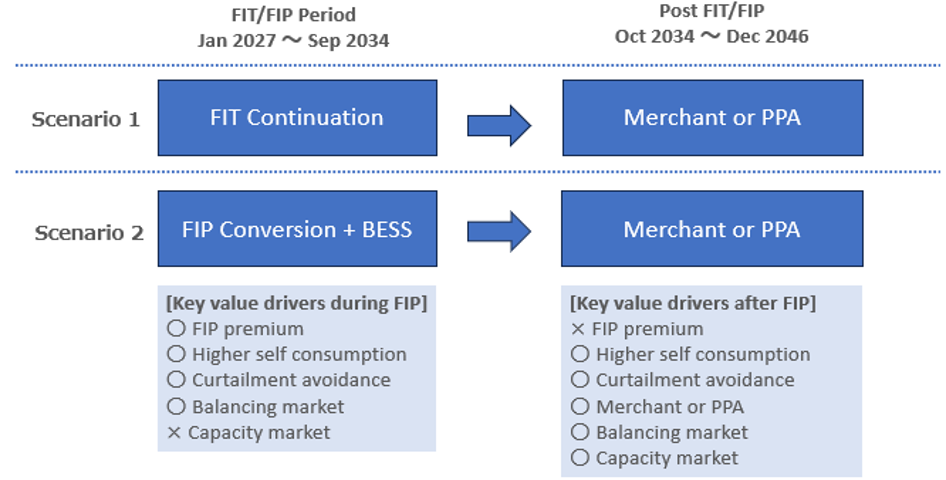

(Figure 1: Conceptual comparison of FIT continuation versus FIP conversion with battery storage)

1. Assumptions

The analysis is based on a publicly announced rooftop solar project in the Kyushu region that plans to convert from FIT to FIP while adding battery storage.

The project assumptions include:

* Solar PV capacity: approximately 1.5 MW

* Battery power rating: 2.56 MW

* Battery energy capacity: 8.94 MWh

The project originally received FIT certification in FY2013 at a tariff of JPY 36/kWh. We assume that the project converts to FIP and commissions the battery system in 2027. After the FIT/FIP support period expires in September 2034, electricity is assumed to be sold either directly into the wholesale market or through a corporate PPA arrangement.

The analysis covers a 20-year period from 2027 to 2046 and assumes that the battery participates in:

* Wholesale electricity market arbitrage

* Balancing market services

* Capacity market participation

Based on the assumptions disclosed for the reference project, self-consumption is assumed to increase by 10% compared with the current level.

The following two scenarios were evaluated:

*Case 1: Continue under FIT

*Case 2: Convert from FIT to FIP and install battery storage

2. Results

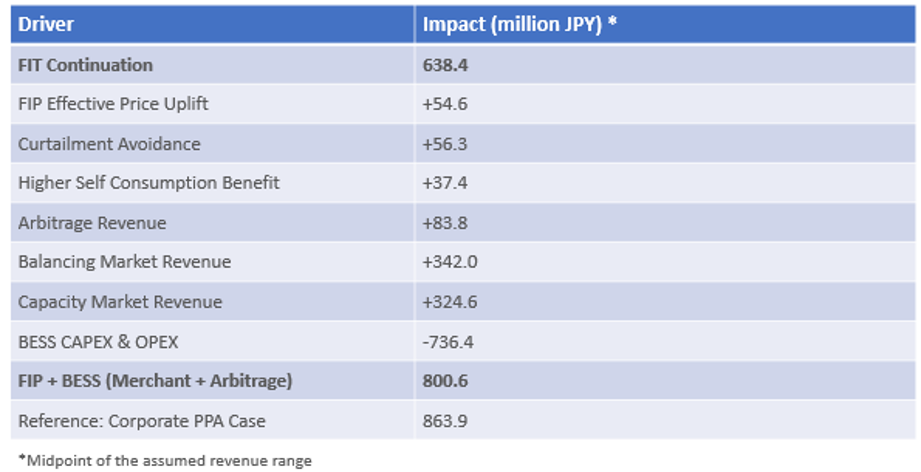

The estimated cumulative project revenues over the 20-year analysis period are as follows:

* Case 1: FIT continuation → approximately JPY 640 million

* Case 2(1): FIP + Battery (Merchant Market Model) → approximately JPY 800 million

* Case 2(2): FIP + Battery (Corporate PPA Model) → approximately JPY 860 million

Under the assumptions used in this analysis, the FIP conversion and battery storage scenarios generated higher revenues than continuing under FIT.

Furthermore, the corporate PPA case outperformed the merchant market case after the expiration of the FIP support period. Both cases assume participation in the balancing market and capacity market.

It should be noted, however, that the results are highly sensitive to assumptions regarding future market prices and regulatory conditions.

(Figure 2: Comparison of FIT continuation, FIP + Battery (Merchant Model), and FIP + Battery (Corporate PPA Model))

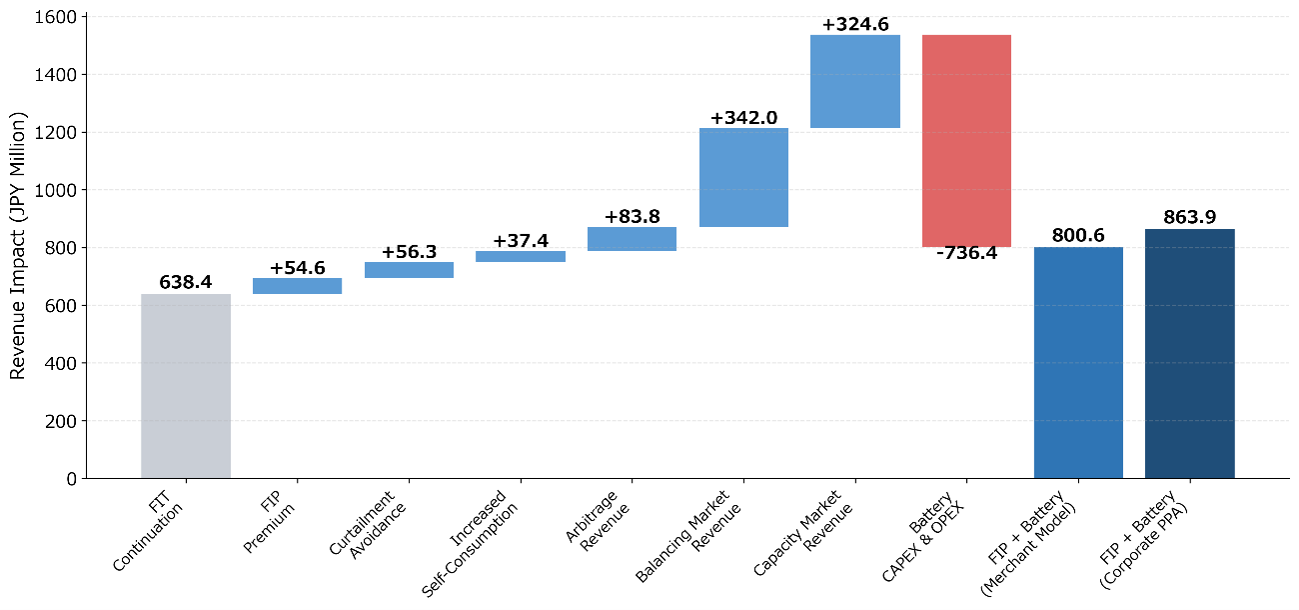

3. Key Value Drivers

What creates value when a project converts from FIT to FIP and installs battery storage?

In this analysis, the following sources of value were considered:

* Revenue enhancement from FIP conversion

* Avoided renewable curtailment

* Increased self-consumption

* Wholesale market arbitrage

* Balancing market participation

* Capacity market participation

The largest contributors to improved project economics were balancing market revenues and capacity market revenues.

Although FIP conversion and curtailment mitigation provided measurable benefits, their contribution to total project value was relatively modest compared with the revenues generated through battery-enabled market participation.

The results suggest that the economic attractiveness of FIT-to-FIP conversion combined with battery storage depends less on the FIP mechanism itself and more on the ability of the battery system to access multiple market revenue streams and on future electricity market conditions.

(Figure 3: Value Driver Analysis)

4. Important Considerations

The results presented here are based on a specific set of assumptions and should not be interpreted as guarantees of future project performance.

Project economics can vary significantly depending on factors such as:

* FIP premium levels

* Wholesale electricity prices (including solar capture prices)

* Corporate PPA prices

* Balancing market prices

* Capacity market prices

* Renewable curtailment rates

Consequently, the findings cannot be generalized across all projects. Detailed analysis is required for each individual project, taking into account regional characteristics, project-specific assumptions, and expected market conditions.

5. Conclusion

In the case examined here, converting an existing FIT project to FIP and adding battery storage demonstrated economic viability under a reasonable set of assumptions.

Perhaps the most important finding is that the primary source of additional value was not the improvement in revenues associated with FIP conversion itself, but rather the new revenue opportunities enabled by battery participation in multiple electricity markets.

As renewable curtailment becomes more frequent and increasing numbers of FIT projects approach the end of their support periods, FIT-to-FIP conversion combined with battery storage is likely to become an increasingly attractive option.

However, project economics remain highly dependent on regional conditions, project-specific assumptions, and future market prices.

While FIP conversion and battery storage can significantly expand revenue opportunities, they also require project owners to relinquish the price certainty provided by the FIT scheme and assume greater exposure to market risk.

コメント